© werner de coster dreamstime.com

Electronics Production |

Developing trends – Part 2: The EMS cluster shuffle?

In the last article, we investigated the drivers of electronics manufacturing cluster development and studied some examples in China, the world’s primary region for electronics manufacturing.

EDITOR'S NOTE_ All images have zoom function. All images © Riverwood Solutions.The investigation showed how a host of changing factors over the past five years has spurred cluster development in several interiorly located Chinese regions. In this article, we explore the question of whether these factors could catalyze a sustained migration of electronics suppliers from present clusters along China’s developed coast to these new interior clusters. We also examine if the same factors could spur new cluster development in other parts of Asia. A combination of factors drive cluster development and each factor weighs differently depending on the situation. While labor cost is a critically important factor, taken alone it probably is not sufficient to spur a migration away from Shenzhen or Shanghai. Dramatically lower labor costs can be found in a number of areas throughout China and Southeast Asia, but new clusters in Chongqing, Chengdu, and Henan have only blossomed in the last 5 years. Arguably the most important factor in electronics manufacturing cluster development is the existing density and volume of electronics suppliers in the cluster. The larger the cluster, the more valuable it becomes. This snowballing phenomenon generates an increasingly powerful supply chain, so only a combination factors will lure suppliers to new manufacturing locations over supplier-dense meccas such as Shenzhen and Dongguan.

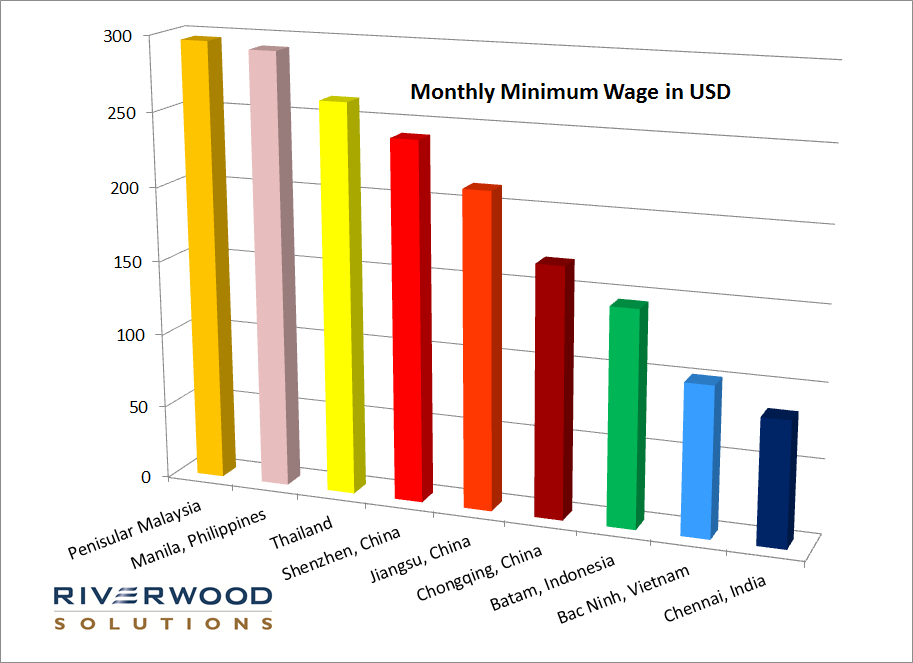

Moving to Inland China – The Time is Ripe As we began to see in the last article, this is precisely the situation that has developed in China. In addition to lower labor costs, a larger supply of labor exists in interior China; it is from these inland provinces that most of the migrant workers originate. Previously, establishing operations in interior China near the large labor supply was impractical due to infrastructure weaknesses. However, many of these areas are now logistically feasible to operate in due to recent rapid and massive infrastructure development. But workers have been willing to temporarily migrate long distances to staff factories in Shenzhen and Shanghai, partially negating the lure of lower labor costs in the interior. More recent developments suggest that worker willingness to migrate may be on the downturn. Increased worker unrest in factories, high turnover rates, and labor supply shortages necessitating greater use of university interns on the factory floor indicate a disruption in the steady supply of migrant labor. The potential for higher earnings at faraway factories may no longer be sufficient enough to overcome the sacrifice many Chinese workers make in relocating to electronics manufacturing clusters. Through the Hukou system, which is tied to an individual’s legal residence and typically inherited, workers and their families receive social benefits, but only in the area of their legal residence. The Hukou system was instituted in 1958 to control mass movement from rural to urban areas, but later reforms loosened the system, allowing temporary migrant labor to flourish. However, when workers migrate to a faraway factory town, they lose these social benefits. The value of these benefits, along with more employment opportunities in interior China, is slowing the flow of migrant workers. For the electronics supplier, faced with a shortage of migrant labor, relocating or adding capacity in inland China is now a real option. Slap on some meaningful tax breaks from the local government and notice a burgeoning class of new consumers in the inland provinces and suppliers start moving. Foxconn, Flextronics, Cisco, Intel, Quanta and many others now have manufacturing in Chongqing, Sichuan, Henan, Guangxi and Shanxi. However, these new electronics manufacturing clusters will not replace Shenzhen and Shanghai. The most important factor for an electronics manufacturing cluster is a dense concentration of electronics suppliers. The existing supplier networks, infrastructure, proximity, and relationships create a powerful supply chain and enormous value for the overall manufacturing cluster. New clusters in interior China may steal some growth potential from the coastal clusters as new capacity is added in the interior and regional specialization becomes more ubiquitous, i.e. laptops in Chongqing, tablets in Chengdu. But the Pearl River Delta and the area around Shanghai will be centers of electronics manufacturing in China for a long time. The strategic locations and manufacturing infrastructure of these clusters allow for efficient manufacturing. Widespread component availability enables short lead times, while nearby testing, assembly and logistics service suppliers bring fluidity to the entire manufacturing process. Product moves quickly overseas, facilitated by nearby port access.Figure 1: Minimum wages in selected areas.

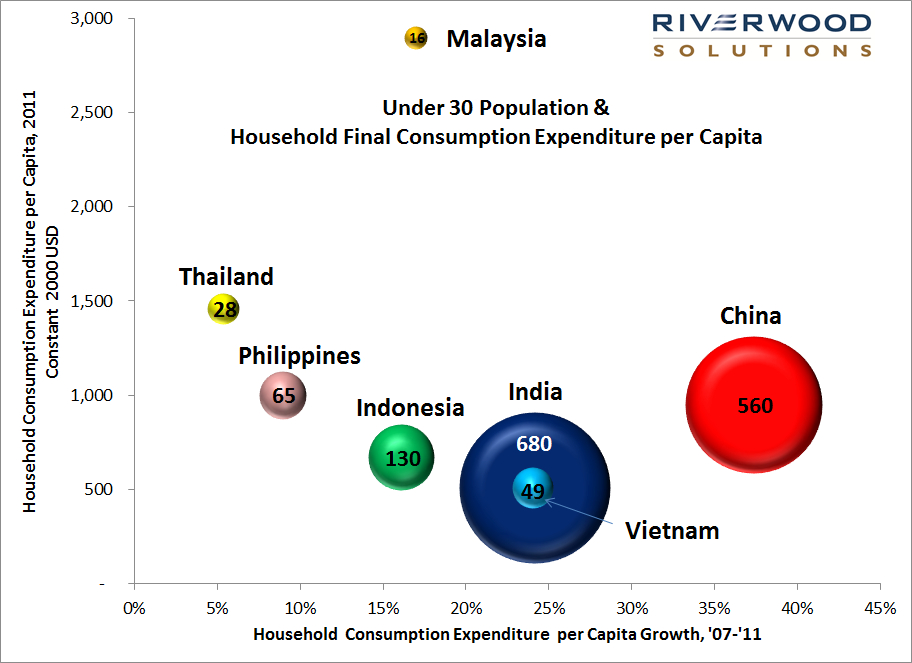

Manufacturing for Domestic Consumption – A New Model? There is a lot of focus in the media on rising labor costs in China and the growing attractiveness of lower costs regions in other parts of Asia. Some have forecast a migration of electronics manufacturing out of China and into these regions. To analyze this idea it is useful to first make a general distinction between different types of electronics manufacturing: manufacturing for export and manufacturing for domestic consumption. Traditionally, electronics manufacturing in developing countries such as China and Malaysia was primarily for export to wealthier, developed nations with large consumer bases and deep pockets. However, developing countries unsurprisingly tend to develop, and with that so do their consumers’ appetites for electronics. China’s rapid income growth is creating a huge domestic market, causing the proportion of electronics manufacturing in China for domestic consumption to grow relative to that for export. The same phenomenon of brisk income growth is occurring in other Asian nations with large populations, such as India, Indonesia and Vietnam. The interesting question that jumps out is: where will the manufacturing that supplies these large developing markets reside? Can China ramp up its manufacturing engine to meet the demand of its existing customers in developed nations, its own expanding consumer base, and the growing markets in South Asia? Figure 2 above shows domestic market size and consumption trends in developing Asian nations. This demographic is assumed to have the largest future electronics products consumption potential. China, with its large under-30 population, higher consumption expenditure, and strong growth leads this group as a market for electronics products. However, Indonesia and India will also become enormous markets if consumption expenditure continues to grow at current rates. China may not have the capacity to supply these additional markets without significant increases in labor availability and productivity, which would result in higher manufacturing costs. Even now there are reports of labor shortages at factories that result in alleged use of underage labor. Another concerning factor is China’s population demographic, which is skewed towards an aging population that will experience greater retirement rates in future years. Without more factory automation, it could be very difficult to develop the necessary capacity to supply the up and coming electronics markets in South Asia.Figure 2: Consumption potential by country. This chart shows per capita consumption and per capital consumption growth from 2007-2011. Bubble size represents the country’s under-30 population in 2011.

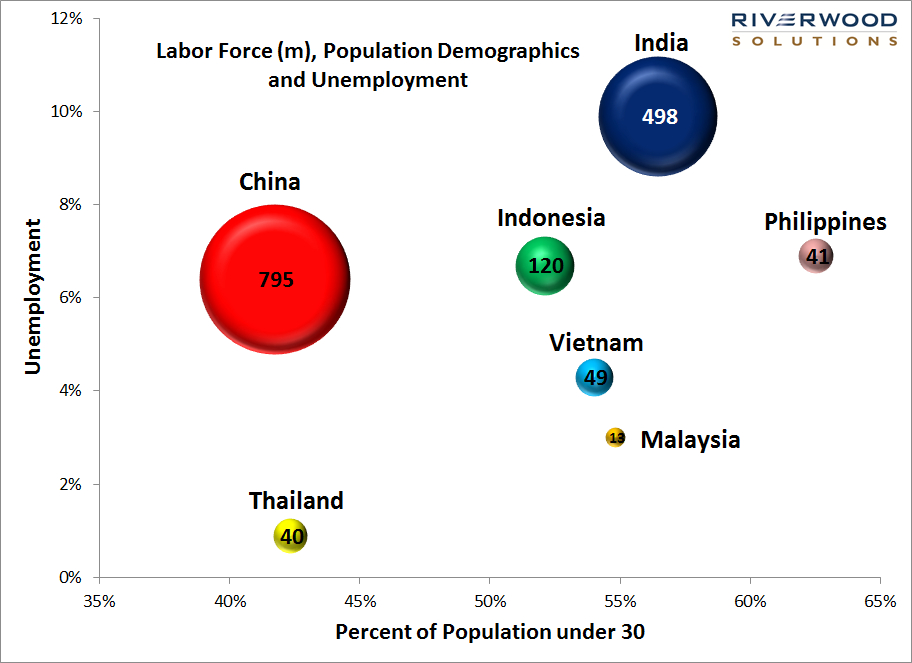

A more practical path could be for new electronics manufacturing clusters to develop that primarily serve their domestic markets, while China continues to support demand in wealthy, developed markets. Some of the South Asian countries with big and growing domestic markets also possess large labor supplies and young populations that could potentially fuel electronics manufacturing clusters that serve their domestic markets. In figure 3 above, notice the difference in labor supply demographics between China, India, and Indonesia. While China’s labor force is much larger, 58 percent of its population is over 30 years old and its unemployment rate is 6 percent. As China’s aging population begins retiring from the workforce, the labor supply will grow more slowly and unemployment will fall, challenging already short-staffed factories. India and Indonesia both boast populations where over 50 percent of the people are less than 30 years of age. Their labor supplies will grow more quickly in the coming years. From a staffing perspective, quickly ramping up factories in India or Indonesia could be a more effective solution to meet rising domestic demand or a new product launch, such as one similar that of an Apple product release; an I-Phone 5 factory ramp-up reportedly fell short by 30 thousand workers last year. Building capacity in other countries might relieve China’s labor market to focus on production that meets the growing demand of its own consumers, while it continues to dominate outsourced manufacturing.Figure 3: Current and future labor supply. This chart shows the labor supply, unemployment rates and the percent of the population under 30 years of age for 2011.

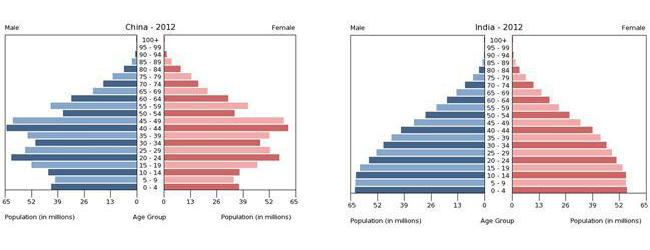

Foxconn is presently in negotiations to establish manufacturing in Indonesia (rumored to be in Serang, Banten). An issue that has allegedly delayed Foxconn’s Indonesian site is governmental regulations that do not do enough to prevent counterfeit mobile phones from entering the Indonesian market. This indicates Foxconn’s intention to manufacture for the domestic market, at least initially. The pending investment in Indonesia is speculated to be as high as USD 10 billion. Flextronics, Beyonics and several other suppliers also have manufacturing in Indonesia, many in Batam. In India, Foxconn, Flextronics and Jabil operate facilities in Jaipur, Chennai and Mumbai. Relocation of Outsourced Manufacturing – More of an Exception Indonesia, India, and other growing locations for electronics manufacturing cluster development do qualify as having lower labor costs relative to China (see figure 1). However, rather than being the justifying factor for new clusters to develop, lower labor costs lend credence to the manufacturing location decision. If labor costs were the only factor, electronics suppliers would all move to India. Clearly that has not happened. When lower labor costs combine with another factor, such as proximity to an existing cluster, then suppliers may relocate from China to another country to serve export markets. For example, Foxconn established manufacturing in northern Vietnam in 2010 and presently operates five facilities in Bac Giang and Bac Ninh provinces. These locations lie on the border of southern China, very close to the cluster in Guangdong and the planned Foxconn location in Nanning, Guangxi province. The Foxconn facilities in Vietnam complement the Foxconn facility in Shenzhen and have become part its production network. Labor costs in these Vietnamese provinces are favorable relative to those in Shenzhen and almost all of China. These lower labor costs combined with the close proximity to an existing cluster made this a valuable location. Furthermore, China and Vietnam have reached an agreement to build a highway between nearby Hanoi and Shenzhen that will ease restrictions on trucks travelling between Guangxi, Guangdong and Vietnam. This improved logistics capability will add even greater value to this developing northern Vietnamese cluster. Conclusion Established electronics manufacturing clusters in China and Malaysia, despite their growing labor costs, will not move to lower cost countries any time soon. The primary value of the cluster is the sheer number and density of electronics suppliers within the cluster – this supplier volume and density creates a network of suppliers with strong relationships that reside within close proximity to one another.Figure 4: Population demographic comparison of China and India. India’s population is skewed towards the young, while China’s population is more middle-aged. Chart from the CIA World Fact book (cia.gov).

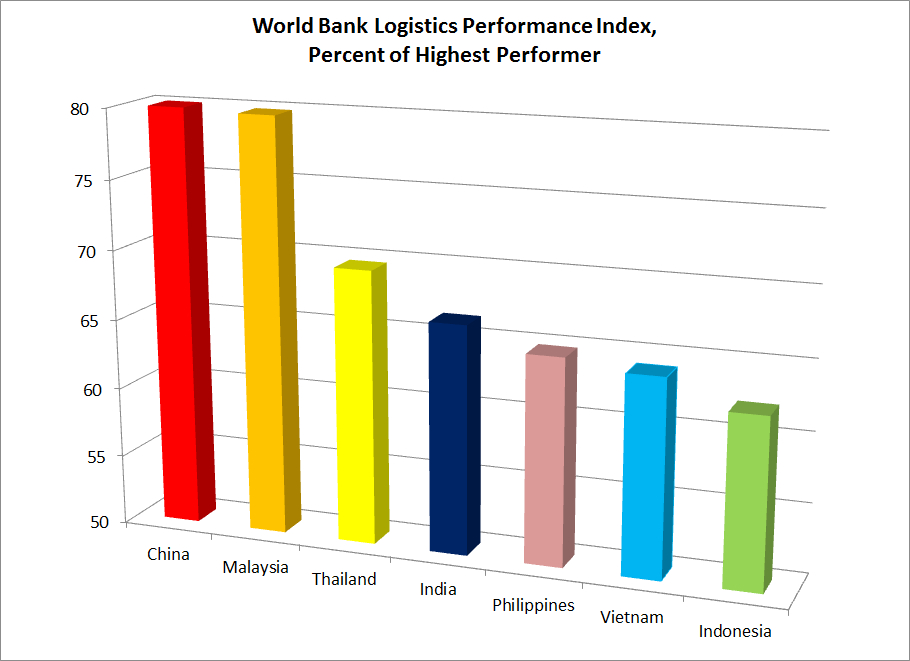

Economies of scale in sourcing, production and logistics all contribute to efficient and cost-effective manufacturing. Only an exceptional combination of critical factors will lead suppliers to relocate. In the case of supplier relocation within China, the combination of factors – labor costs, labor supply, proximity to market, infrastructure development, and investment incentives – are strong enough to spur some relocation to interior regions where clusters are developing. China’s electronics manufacturing capacity may be challenged to efficiently supply developing consumer electronics markets in nations such as India and Indonesia, as China grows capacity to meet the demand of its own blossoming consumer base. New clusters may develop in these nations to primarily serve their domestics markets, taking advantage of their lower labor costs, ample labor supplies, and young populations. Clusters in China and Malaysia will likely continue to dominate outsourced electronics manufacturing, as they have the supplier mass, networks, relationships, and infrastructure in place to do so most effectively. Before new clusters in other Asian countries can become leaders in outsourced electronics manufacturing, they must overcome significant infrastructure development challenges. In the last installment in this series, we share a recent survey of industry participants on their opinions of electronics manufacturing cluster development trends. Again, stay tuned…. ----- Author: Xander Kameny, Operations Consultant at Riverwood Solutions.Figure 5: World Bank Logistics Performance Index (LPI). Bar height is the percent of the highest performer in the overall LPI.